SECR Webinar: Who, Where, What and When

On 17th March 2020, Professor Andrew Geens, Head of CIBSE Certification, hosted a webinar presented by Sebastian Gray, Director at 2EA, on the topic of Streamlined Energy & Carbon Reporting (SECR).

SECR came into effect on 1st April 2019 and applies to all quoted companies and large incorporated unquoted companies that meet two or more of the following:

- At least 250 staff

- An annual turnover greater than £36m

- An annual balance sheet total greater than £18m

Sebastian is a CIBSE registered Low Carbon Consultant and Low Carbon Energy Assessor for non-domestic, an ESOS Lead Assessor and EnMS Specialist.

During the webinar, the following topics were covered:

- Who needs to report under the SECR framework?

- Who is enforcing the regulation of SECR?

- What needs reporting?

- The methodologies to use when reporting.

Please note that your SECR report is submitted through Companies House and the Conduct Committee of the Financial Reporting Council is responsible for monitoring compliance of company reports and accounts.

If you have any questions, please do not hesitate to contact us or view our SECR service packages here.

SECR Webinar: Who, Where, What and When

Video Transcription

Hello and welcome to everyone who’s logged in for this webinar.

Welcome to the “SECR: Who, Where, When” webinar – this is a webinar series of energy-related topics. This one is on an energy reporting area that’s not subject to registration schemes like the ESOS requirements, for example. We thought it may be of interest to many of our low carbon consultants that also work in this area.

So, this afternoon, we’ve got Sebastian Gray discussing this topic. He’s involved with it quite a lot with his company 2EA.

Sebastian is on our LCC register as an EnMS specialist and LCC ops, as well as our ESOS register and he’s also an LCEA and DEC assessor. Just a brief introduction there and, without further ado, I’ll hand over to Sebastian.

Sebastian Gray

Thanks, Andrew. So, welcome everyone thanks for taking the time to listen to this webinar today, hopefully, none of you are self-isolating.

Today we’re going to be looking at the government’s latest reporting framework which is Streamlined Energy & Carbon Reporting or SECR for short. Within this presentation I have covered where SECR has come from, who has to report; including when, how, and through who, and we’ll finish with a look at the breakdown of what needs to be reported. I’ve also included a summary from our own workings of what needs to be covered in your report to kind of give you a bit of a head start.

Who we are

So, a bit about us; as Andrew just said we’re registered with CIBSE, we’ve been going for 11 years but we’ve got about 25 years experience in the company and we specialise in implementing UK and EU legislation across an array of sectors and SECR is our latest one that we’re currently doing since last year.

Where did SECR come from?

So, before we jump into the requirements, a little background on where it came from and its reason for existing. This is a bit of a long one but it’s a good explanation to get history.

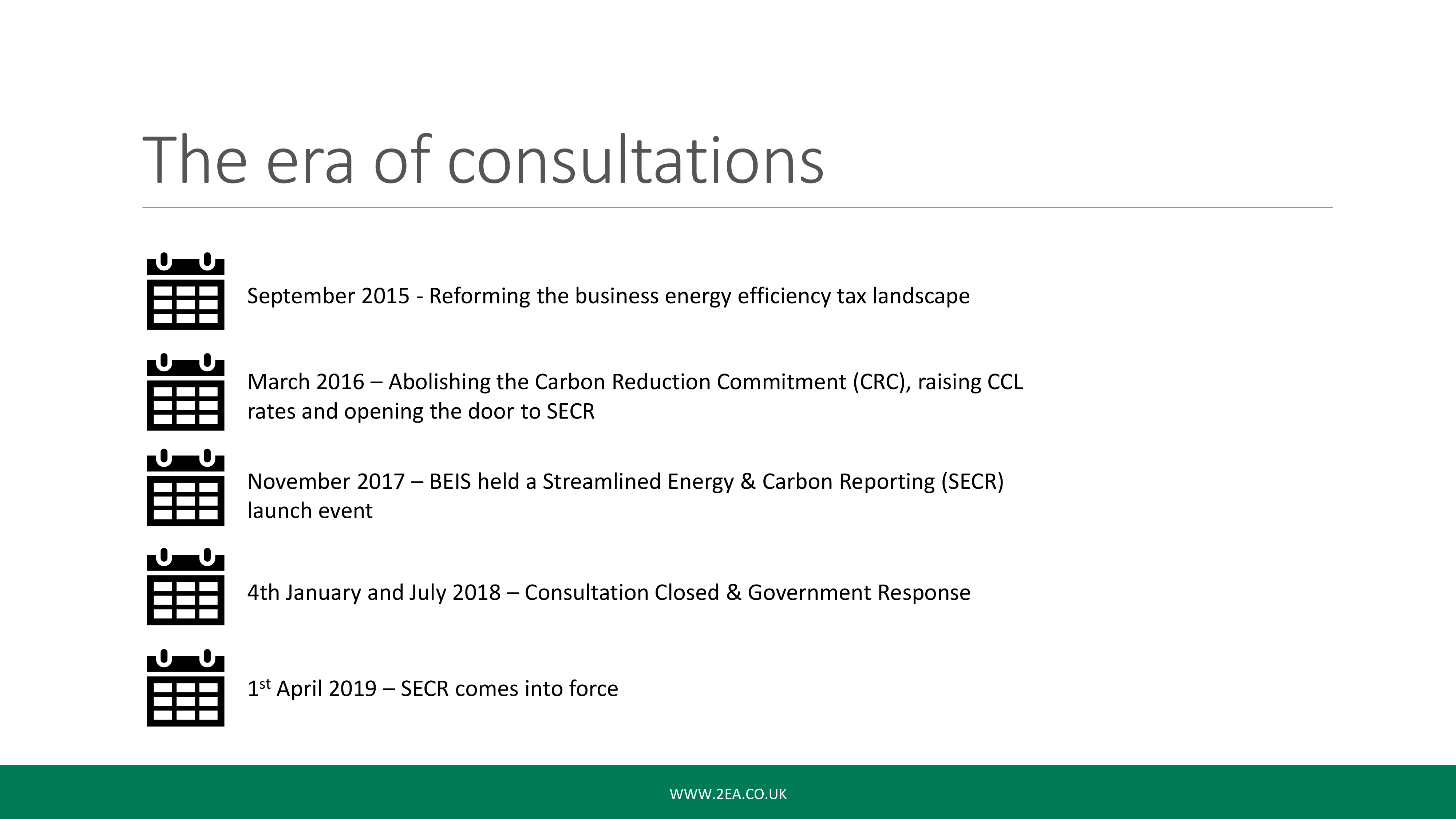

The Era of Consultations

In September 2015 the government put out a consultation called the Reforming the Business Energy Efficiency Tax Landscape (a bit of a tongue twister) and then a consultation response was published in March 2016. It set out the road to abolishing the Carbon Reduction Commitment (CRC) and raising CCL rates to offset this loss.

Within that consultation, there was surprisingly significant support from industry for a mandatory reporting scheme to replace CRC so the government then announced a further consultation, at the time it was called a Simplified Reporting Framework, for introduction in April 2019.

BEIS then launched its consultation in November 2017 for SECR and some of you might have seen it held events at EMEX and at its head office in London Victoria to kind of promote and engage the industry about the upcoming framework.

The consultation then closed on the 4th of January 2018 and, in July 2018, they released their government proposal response introducing SECR. Within this response, interestingly, they found that with CRC ending, CCL rates increasing and the new SECR framework being introduced, there was a net societal benefit of around six hundred and ninety-eight million pounds (£698 million). From there, on the 1st of April 2019, SECR came into force.

You can find it in the Environmental Reporting Guidelines; if you google it, you’ll go straight to a government link – the version you want is version 2 and is dated March 2019 – I spoke to BEIS last week and they have confirmed that there is not yet going to be a version 3.

SECR: Who, What, Where and When

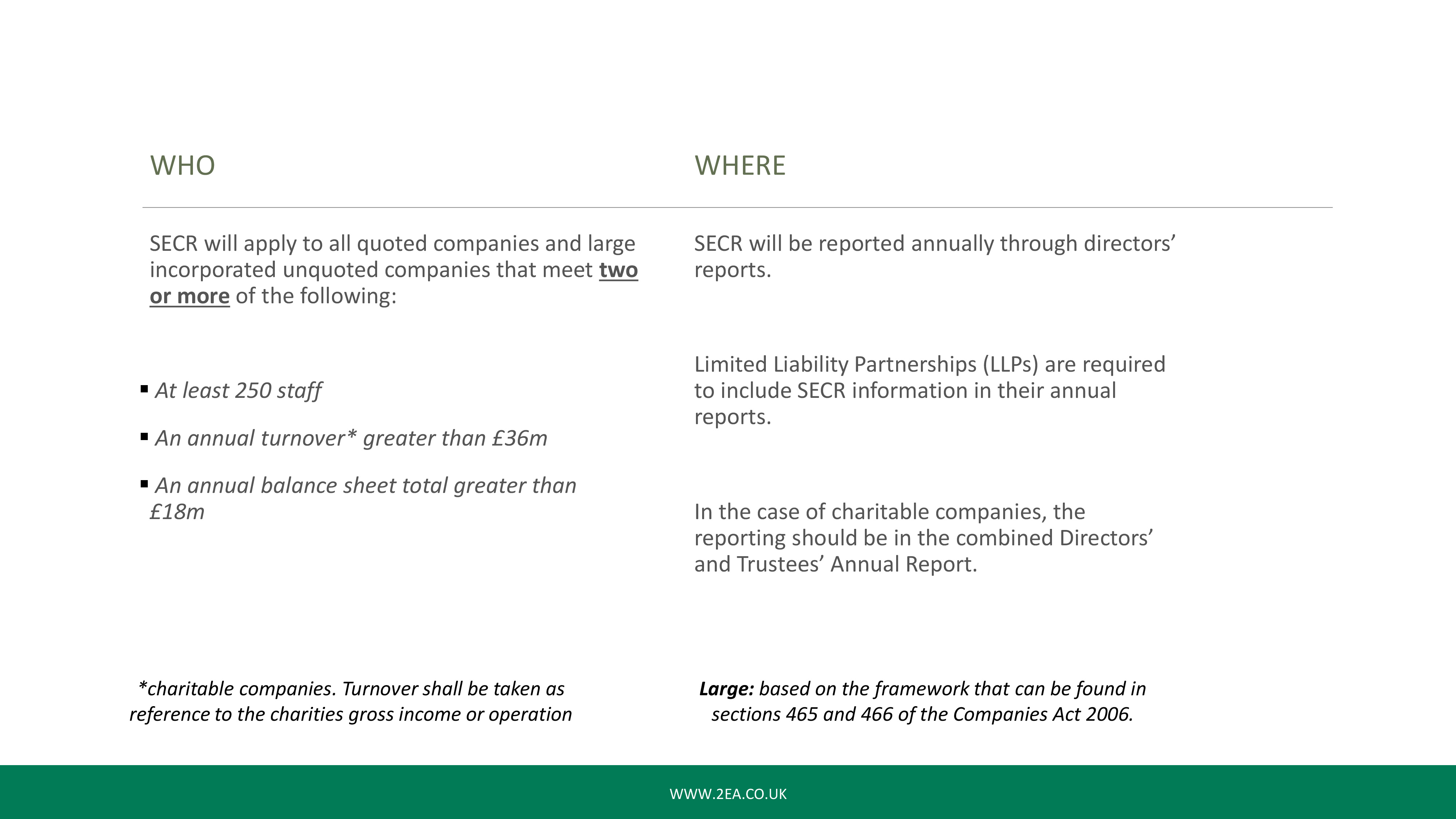

Who: SECR, as it says on the screen, will apply to all quoted companies and large incorporated unquoted companies that meet two or more of the following: at least 250 staff; an annual turnover greater than £36 million; and an annual balance sheet total greater than £18 million.

In relation to turnover for charitable companies, that should be taken as the reference to the charity’s gross income or operation. In relation to quoted companies this, in this respect, is those whose equity share capital is officially listed on the main market of the London Stock Exchange, is officially listed in a European Economic Area State or is admitted to dealing on either the New York Stock Exchange or the NASDAQ.

In relation to where you have to put your SECR report, this goes into Companies House – and if you’re a large incorporated unquoted company, I’ll be saying that a lot. SECR will be reported annually through directors reports. For LLPs it’ll be in their annual reports and in the case of charitable companies, it’s through the combined directors and trustees annual report.

You’ll notice there isn’t a mention of public companies and the reason for that is that most public companies do not have to do SECR. It is a bit of a legal area and I will read what it says in the guidance just to give you an idea of what it does say: “for public companies remember you or parts of your organisation may fall within the scope of SECR even if undertaking public or not-for-profit activities as registered companies or companies/LLPs owned by universities, academic, institutions or NHS trusts. You are, however, not required to report under the SECR framework at an organisational level if your organisation is defined as a public body or contracting authority although you may still have other reporting requirements”.

Basically, what that means is that, if you’re an NHS trust, for example, you’re already following guidelines on the things like the Public Contracts Regulation of 2015 but if you have within the NHS trust a cleaning company and they are a registered company that falls within the requirements of this, then they have to report. As always BEIS does encourage organisations that aren’t in scope to report SECR voluntarily.

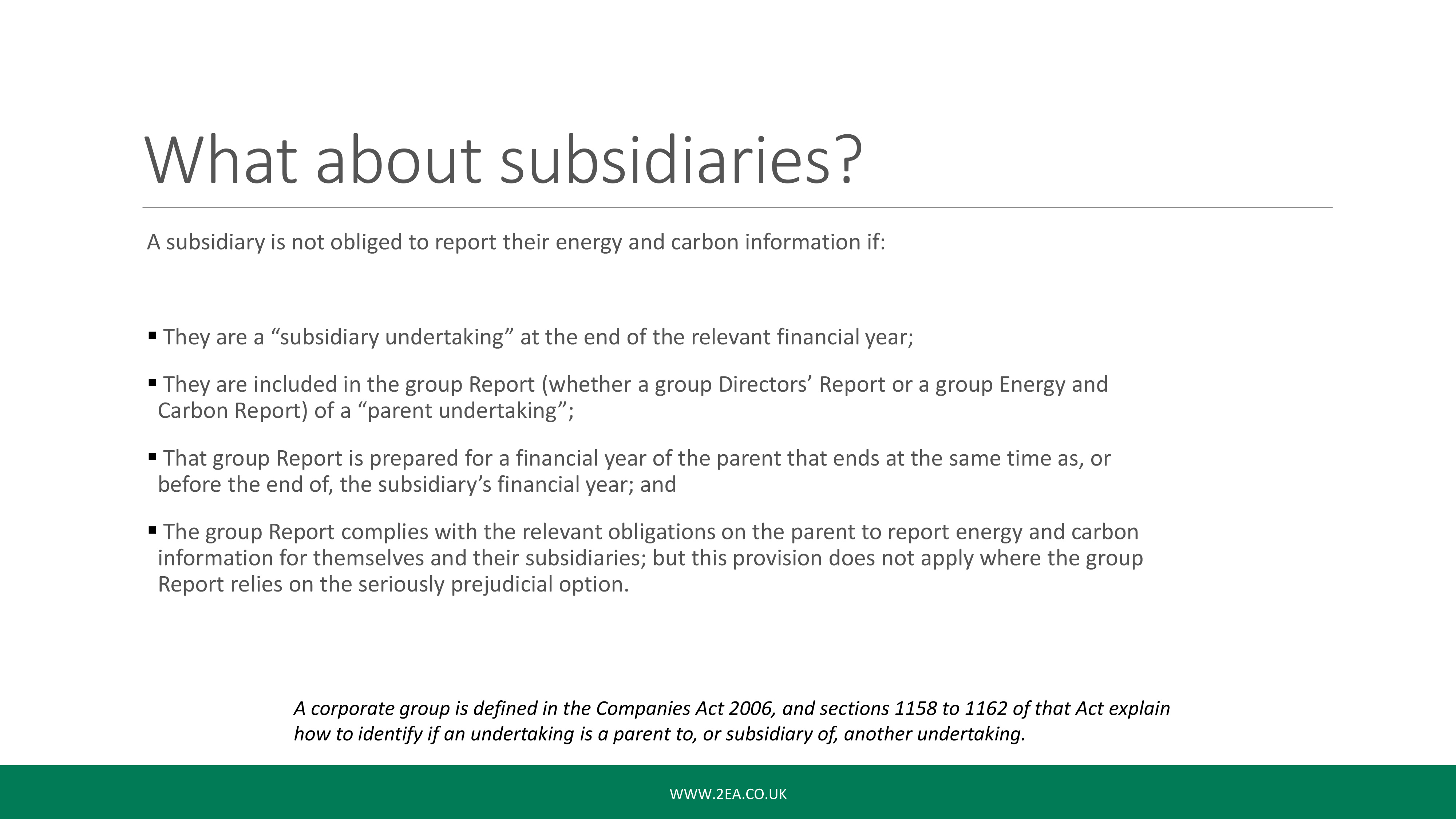

What About Subsidiaries

So, the next slide is about “What about subsidies”. How subsidies report under the SECR framework is different from both ESOS and the closed CRC reporting framework. What’s on-screen is a summary of what subsidiaries are not required to report on the energy and carbon information.

If you are reporting at group level, for a financial period for which you are required to prepare a group directors report. When making your energy and carbon disclosures you must take into account not only your own information but also the information of any subsidiaries included in the consolidation which are all obviously quoted companies, unquoted companies or LLPs.

However, you do have the option to exclude from your report any of the energy and carbon information relating to certain subsidiaries. What that means, is that if you have a company, entity or subsidiary within your corporate grouping which has only 10 employees and a balance sheet or turnover under the threshold, they, in their own right, would not qualify within SECR and you could potentially omit them from disclosure. If you need to fully understand what a corporate group is you can find it in a Company’s Act but you may wish to speak to your finance director as they’ll have more information in relation to how your company framework is structured.

What Needs to be reported?

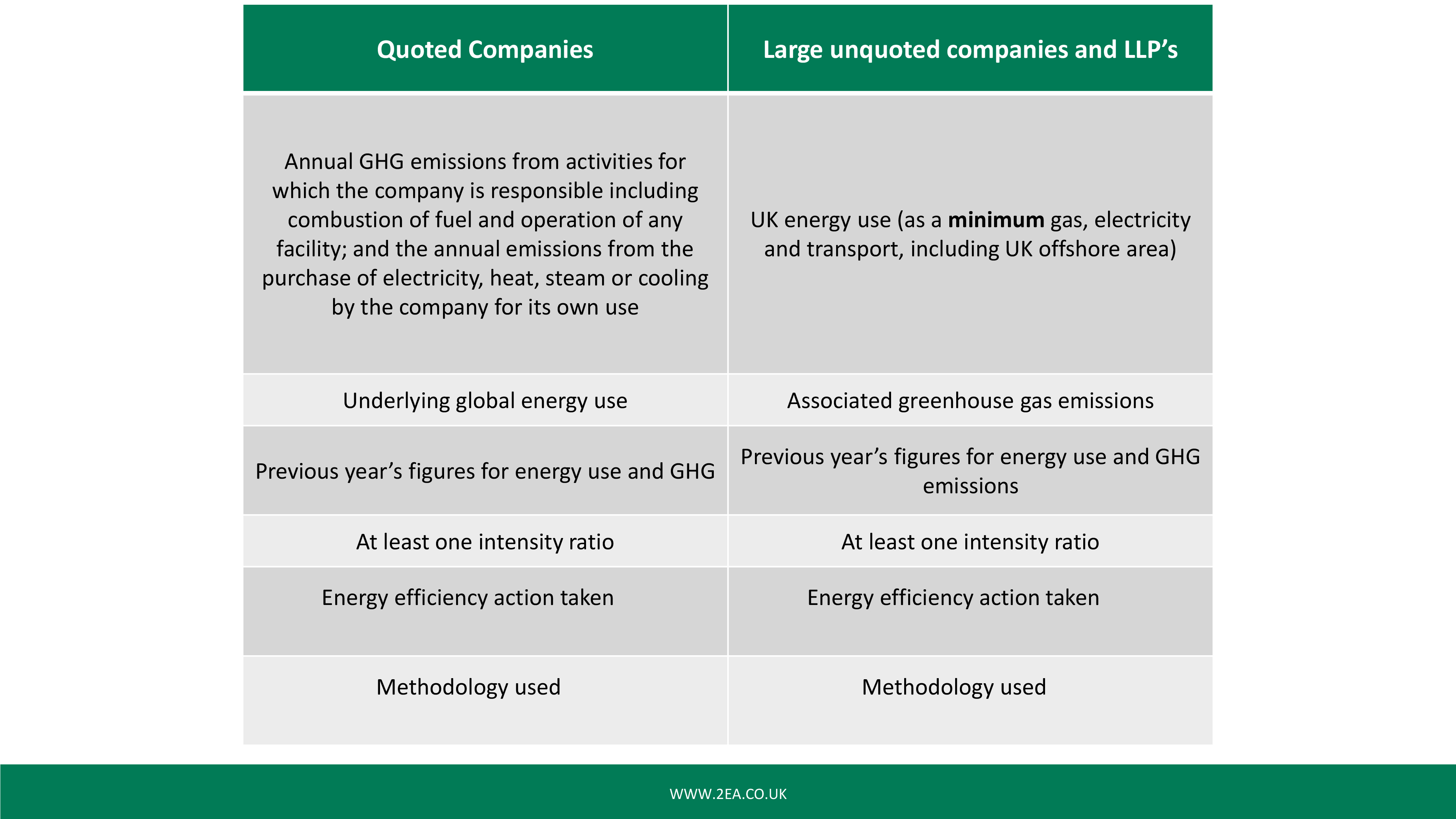

So what needs to be reported? I’ll leave this up for a few seconds while we discuss it. Much of the information you need to complete SECR can usually be obtained from other schemes you participate in and that’s things such as say the closed CRC scheme, ESOS, Climate Change Agreements for some people and the MHGH reporting Framework.

Today we’re mainly focusing on the right-hand column; I am happy to discuss the left-hand column at a later date, but usually quoted companies of such a size have the resources to do this and are already doing most of this reporting in-house, whereas companies that fall into the right-hand column may need a bit more support and clarification. You’ll see that from the third row, what needs to be reported becomes the same across the board regardless.

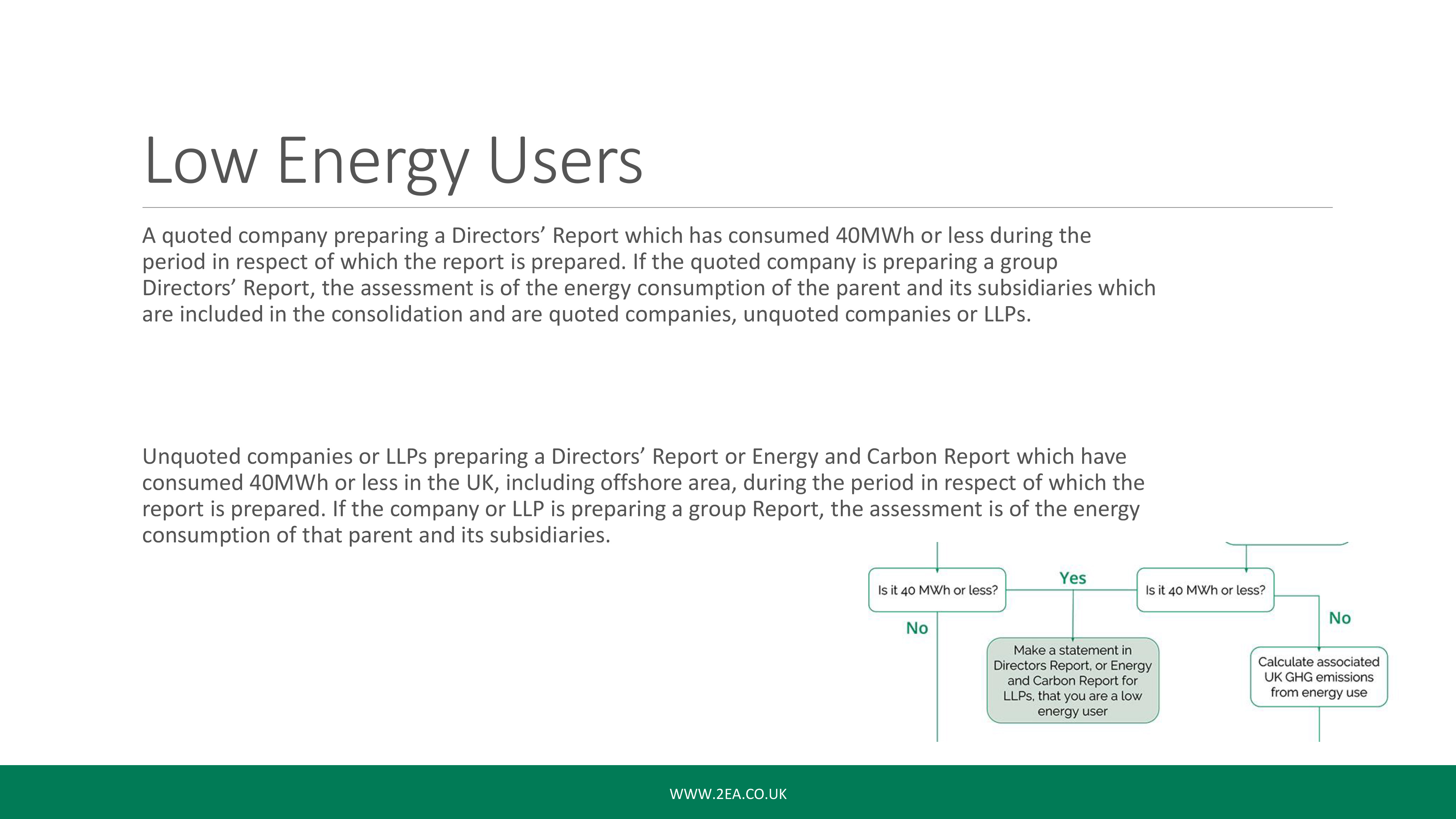

Low Energy Users

The question I know on everyone’s mind is this – do I have to do this? Is there a get out of jail free monopoly card? And to an extent there is. They are called low energy users and it’s pretty much the same for both quoted companies and large unquoted companies. If you found that in your reporting period you consumed 40 megawatts or less within that period, then you’re a low energy user and you just need to make a statement in one of your reports that you are not required to do anything further in relation to SECR. But you must make this statement in your report.

Exclusions from the report

There are exclusions from the reports. Should your organisation find that including any energy and carbon information would be prejudicial to your organisation you can exclude this but, again, you need to make this statement in your report; that you are excluding it for whatever reason. The same goes if you can’t obtain certain energy or carbon information; again, you need to make that statement in your report and include why you weren’t able to gather that information.

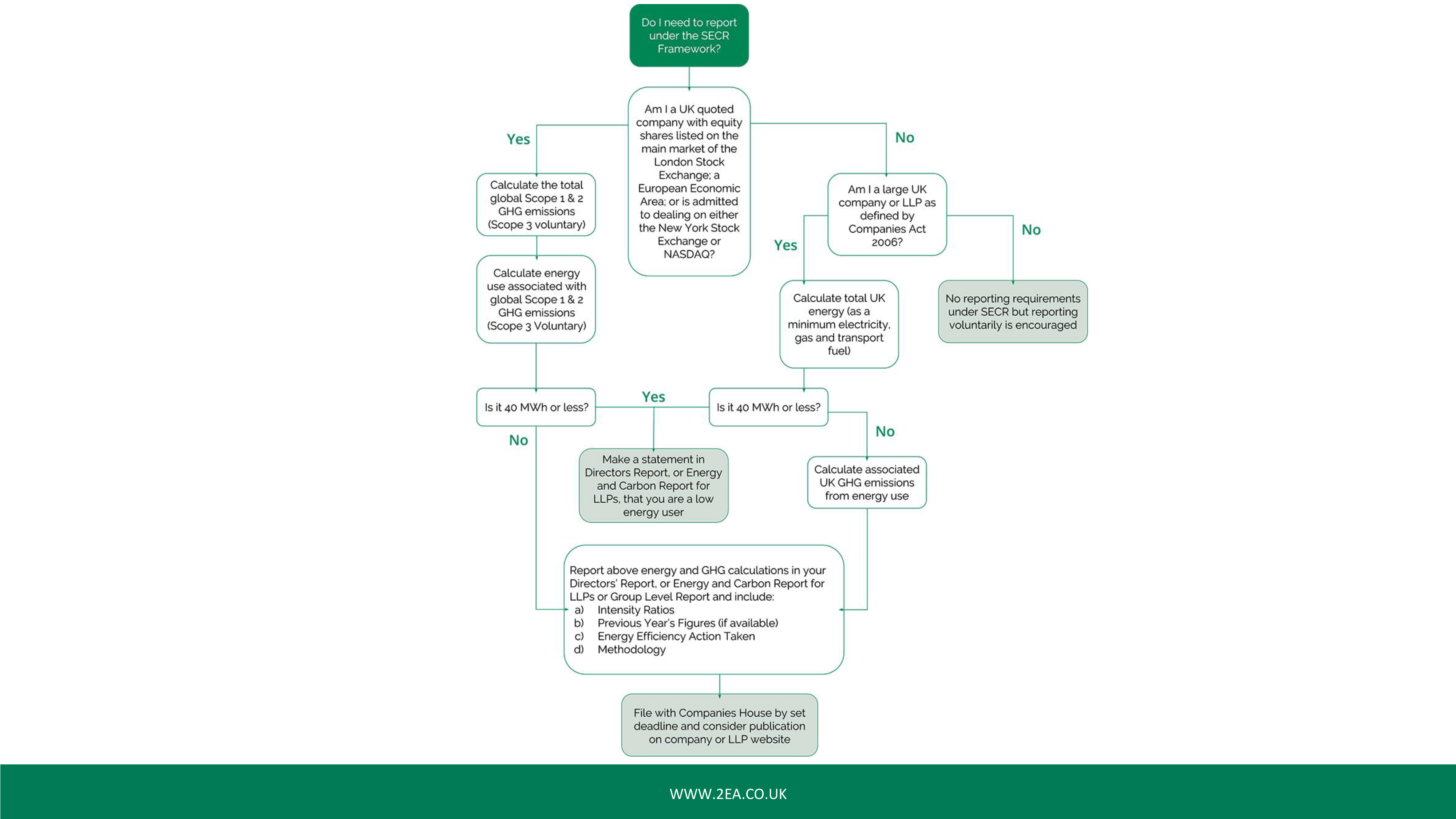

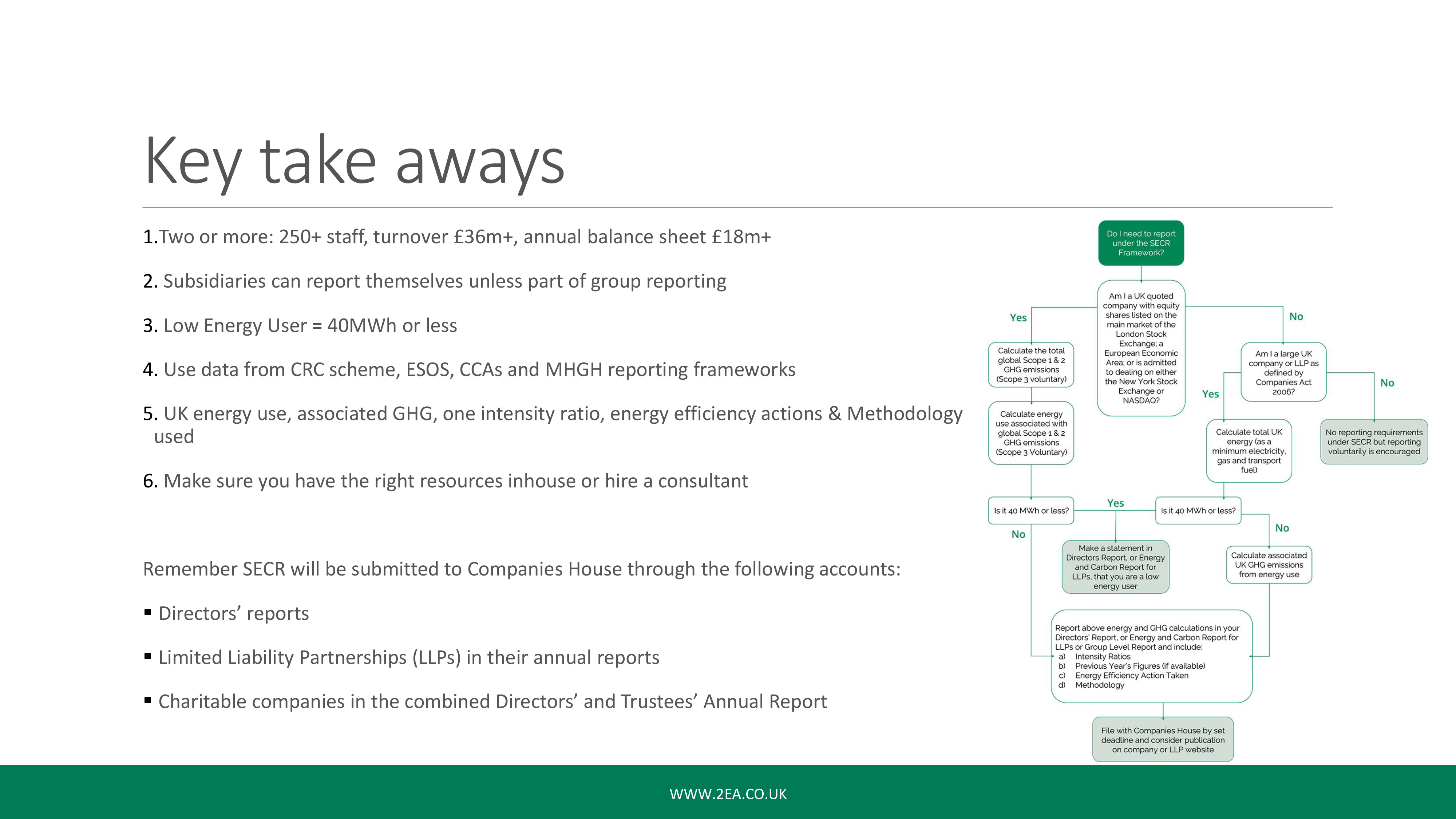

SECR Flow Chart

Before we move on to what needs to be reported, I’ll leave this up for a few seconds so people can get a more visual understanding of whether your organisation needs to report on SECR.

As you can see as we move down we covered whether you’re a quoted company or an unquoted company and then obviously we’re looking again at the right-hand side of the column.

If you are a large company you have to complete SECR if you’re not there’s no requirement but it is voluntary. If you are required, you then have to calculate your total UK energy and we’ll come on to that in a minute.

Once you’ve done that, you find how much energy you are using and if you’re using 40 MWh or less you make a statement in your director’s report, your energy and carbon report for LLPs or the combined report for charities.

If it’s not, then you also then have to calculate your associated UK greenhouse gas emissions which, again, we’ll come on to. You need to put that all into a report and you’ll see there’s A, B, C and D on the screen; we’ll be covering those in a minute. You need to include that in your report and then you’ll see that you file it with Companies House by the set deadline; we’re moving on to that in a minute as well. You’ll notice that there’s no mention of the Environment Agency so far.

When should I report?

So, when should I report? There’s a couple of examples on the screen but I’ll give you a further example: if your reporting year, for example, is November 2018 to October 2019, then your first SECR report period would be November 2019 to October 2020 as it starts after the 1st of April 2019. So, when you’re reporting, you report for the financial year after the 1st of April 2019.

If your financial year is halfway through, and the 1st of April comes in, it’s the next financial reporting year and you do it when you do all of your company accounts at the end of the year.

I should remind people, this is an obligation to disclose annual figures for emissions and energy use and, if you find that your annual period used is not the same as the financial period covered by the relevant report, this must be made clear and BEIS have said that they would like you to align this with your financial year. If you can’t, or do not want to, again you need to make a statement and make this clear in the report.

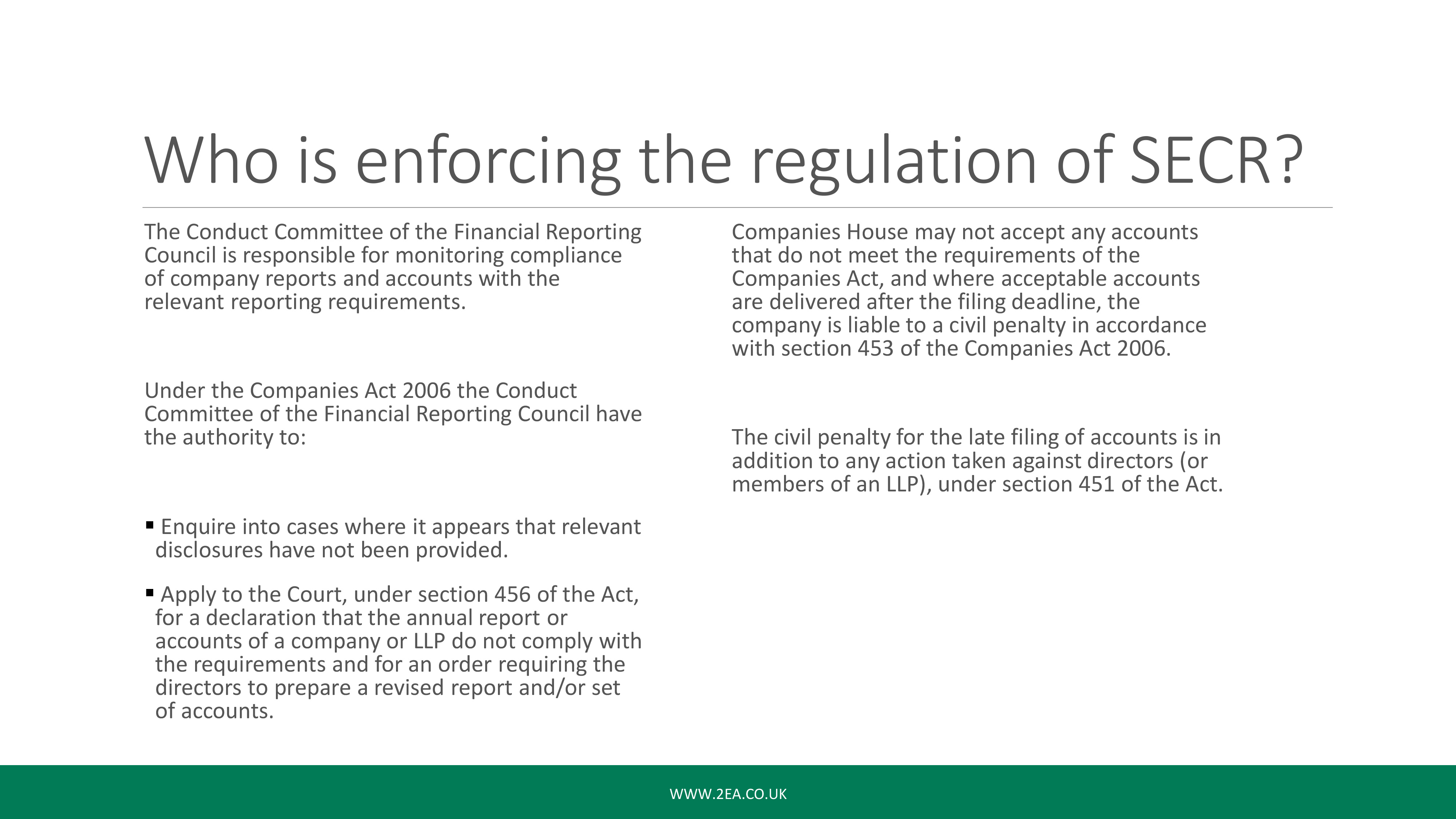

Who is Enforcing the Regulation of SECR?

So, who is enforcing the regulation of SECR? It is not the Environment Agency, it is, in fact, the Conduct Committee of the Financial Reporting Council. While this is obviously rolling out in the first year and the second year is happening, the government will work with Companies House and the Financial Reporting Council to support implementation and to monitor how organisations are responding to these new reporting requirements as part of its overall responsibilities to review the impact of the legislation.

And, again, like I said, it’s not the Environment Agency so the way in which it will be handled is a lot different to what we’ve seen with say ESOS or Climate Change Agreements, for example. As far as possible, the Conduct Committee does operate by agreement with businesses whose reports it reviews. I have had a look into this and to date, it has achieved its objectives without any recourse to the courts.

The committee does exercise its functions with regard to principles of good regulation and it does raise concerns with companies where there is evidence of apparent substantive non-compliance. So, in effect, if you’ve put this report into your end of year reporting and there’s an issue with it, they will let you know and they will work with you to fix this. However, if you don’t do anything and you don’t submit it then obviously they take that a step further.

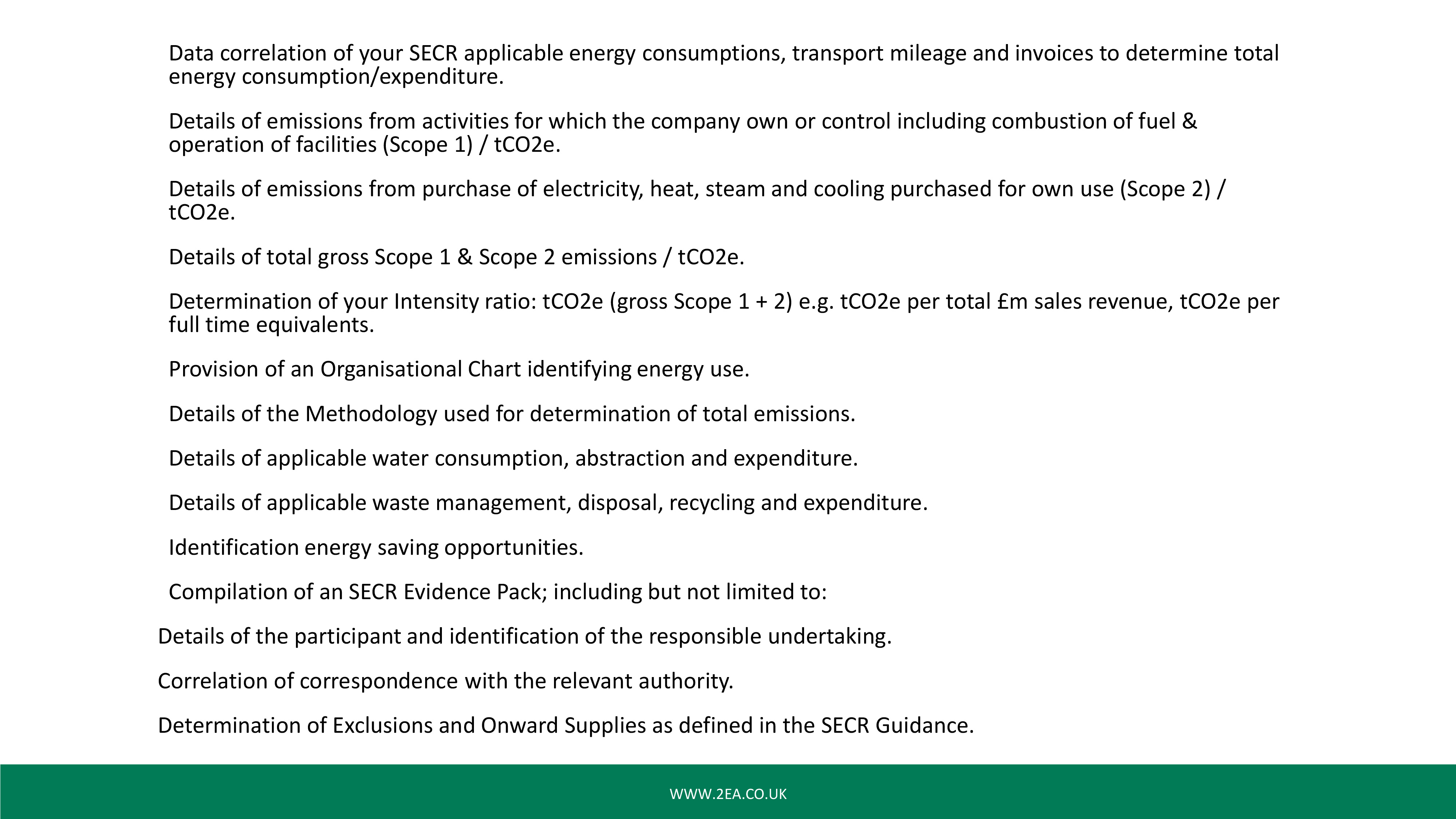

The Information that Needs Reporting

So the information that needs reporting, as I’ve said before, is what’s on the screen in front of you. Again, a lot of this can be found from other reporting schemes and I would say that’s your first port of call for this kind of information, but I’ll go through it; again, I’m covering the right-hand column and I’ll go through each of these, one by one.

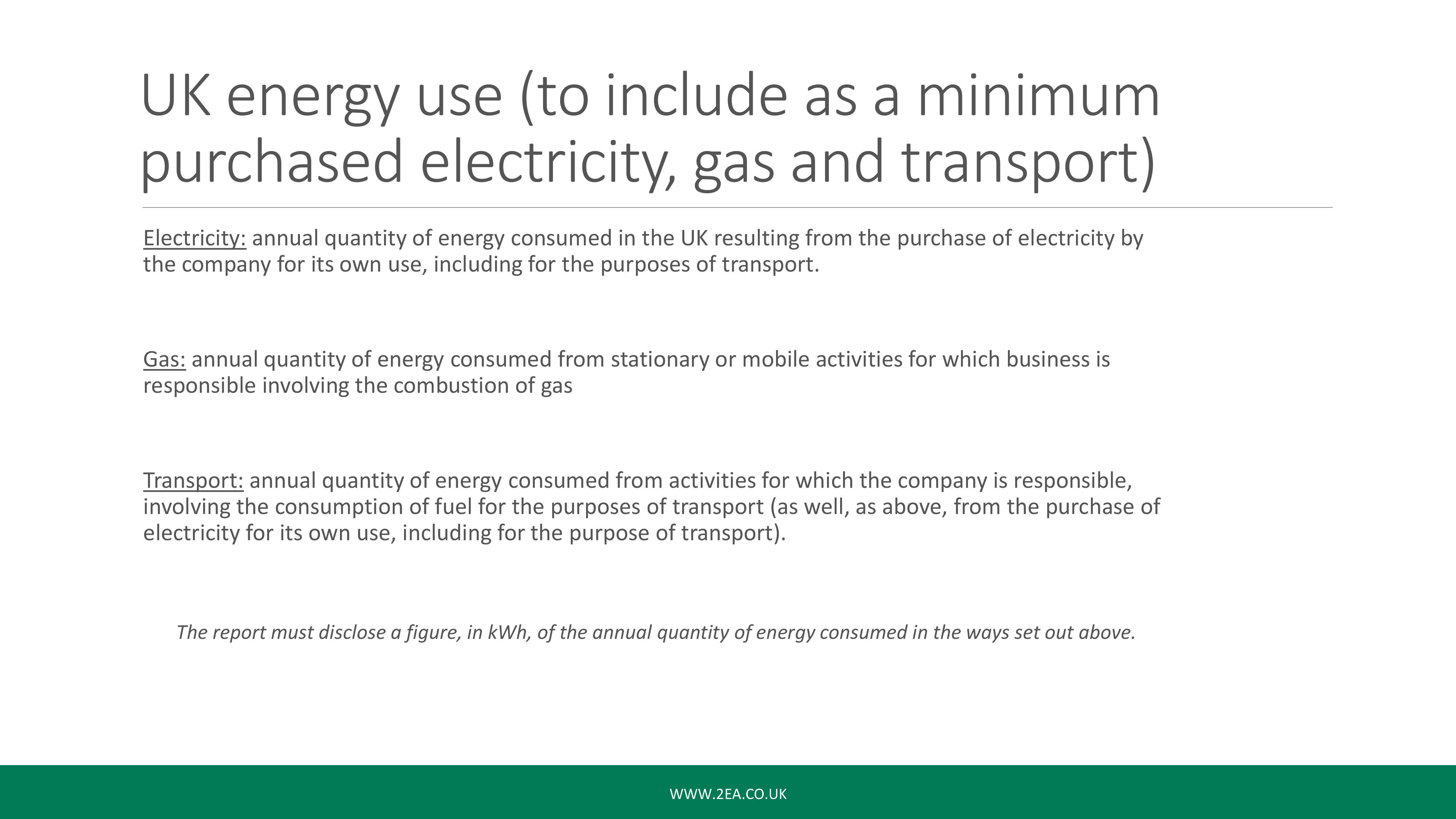

UK Energy Use (to include as a minimum purchased electricity, gas and transport)

So the first one as you can see if we go back is UK energy use and it says adding gas electricity and transport including the UK offshore area. So, again this is very, very similar. This part of it is very similar to the data you take for ESOS and the transport data that you’ll need is based on the same requirements that are reported in ESOS. So if you go and have a look at the ESOS guidelines you’ll find that the requirements to report on transport are pretty similar to what’s seen here today in SECR.

Some energy that is not in scope is things like unconsumed energy that your organisation does not use or supplies to a third party. It can also include energy consumed outside the UK and it can also include energy consumed for international travel or shipping, again, where the journey does not start or end in the UK.

However, you can, if you wish, include international travel if you do conduct international travel outside of the UK. The main key takeaway from this screen is that the report must disclose the figure in kilowatt-hours of the annual quantity of energy consumed in the way set out above. So when you do report this information it must be in kilowatt-hours.

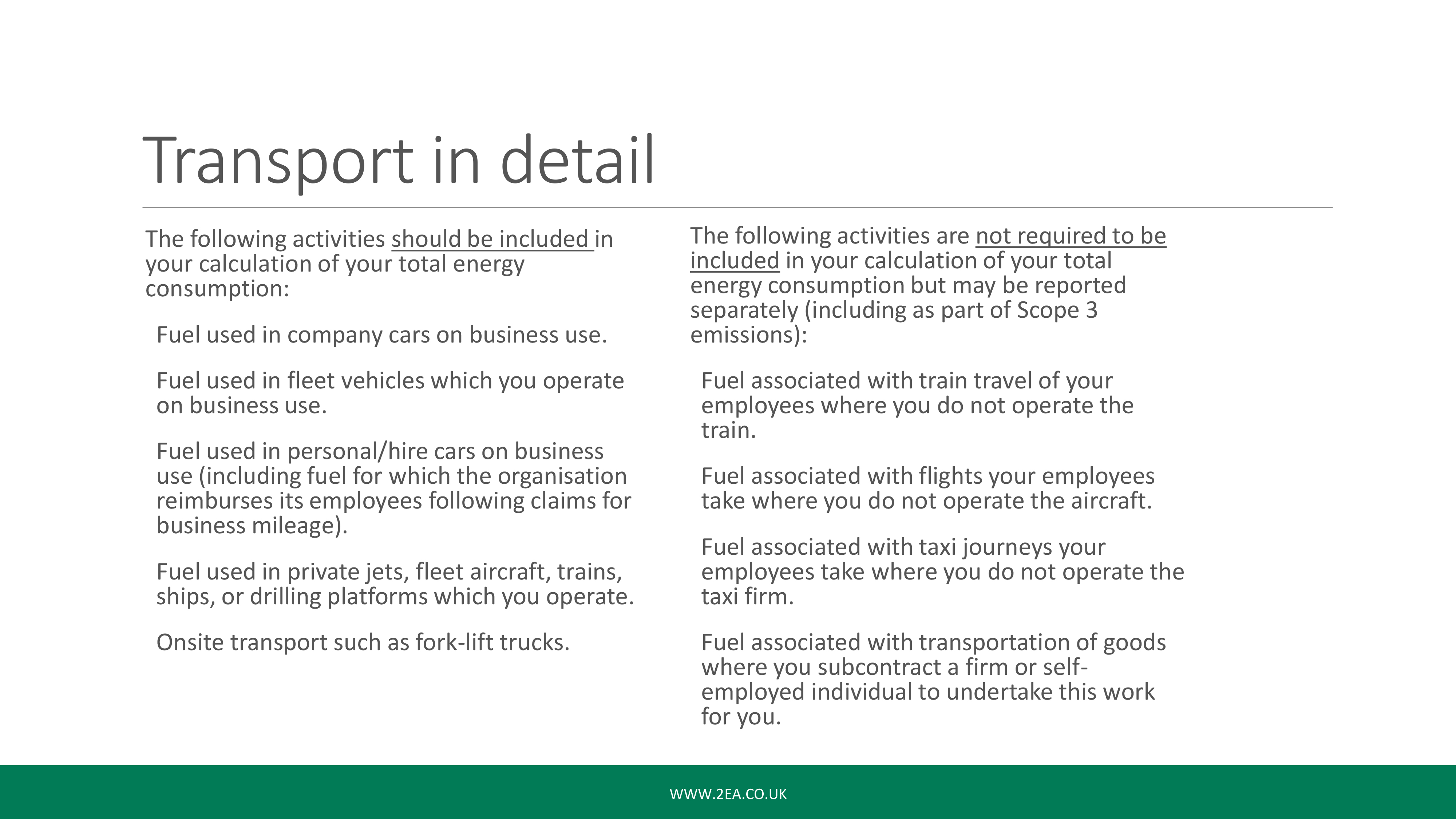

Transport in detail

This screen is here just to breakdown transport in more detail in relation to what should be included, which is on the left-hand side, and the following activities are not required to be included which are on the right-hand side. I’ll leave that up just for a minute so people can have a read through. But, again, it’s very, very similar to the ESOS guidance.

Associated greenhouse gas emissions

Cool. So the next one within that table we were looking at is associated greenhouse gas emissions and this varies for quoted companies and unquoted companies. I’m going to go through these next. I’ve got there in the middle, it says previous year’s figures for energy use and GHG emissions. You don’t have to do this in the first year but you do have to do it in the second, third, fourth and fifth years and so on. You have to include the previous year’s figures – you don’t have to do that first year because obviously there isn’t any unless you are already reporting as a quoted company.

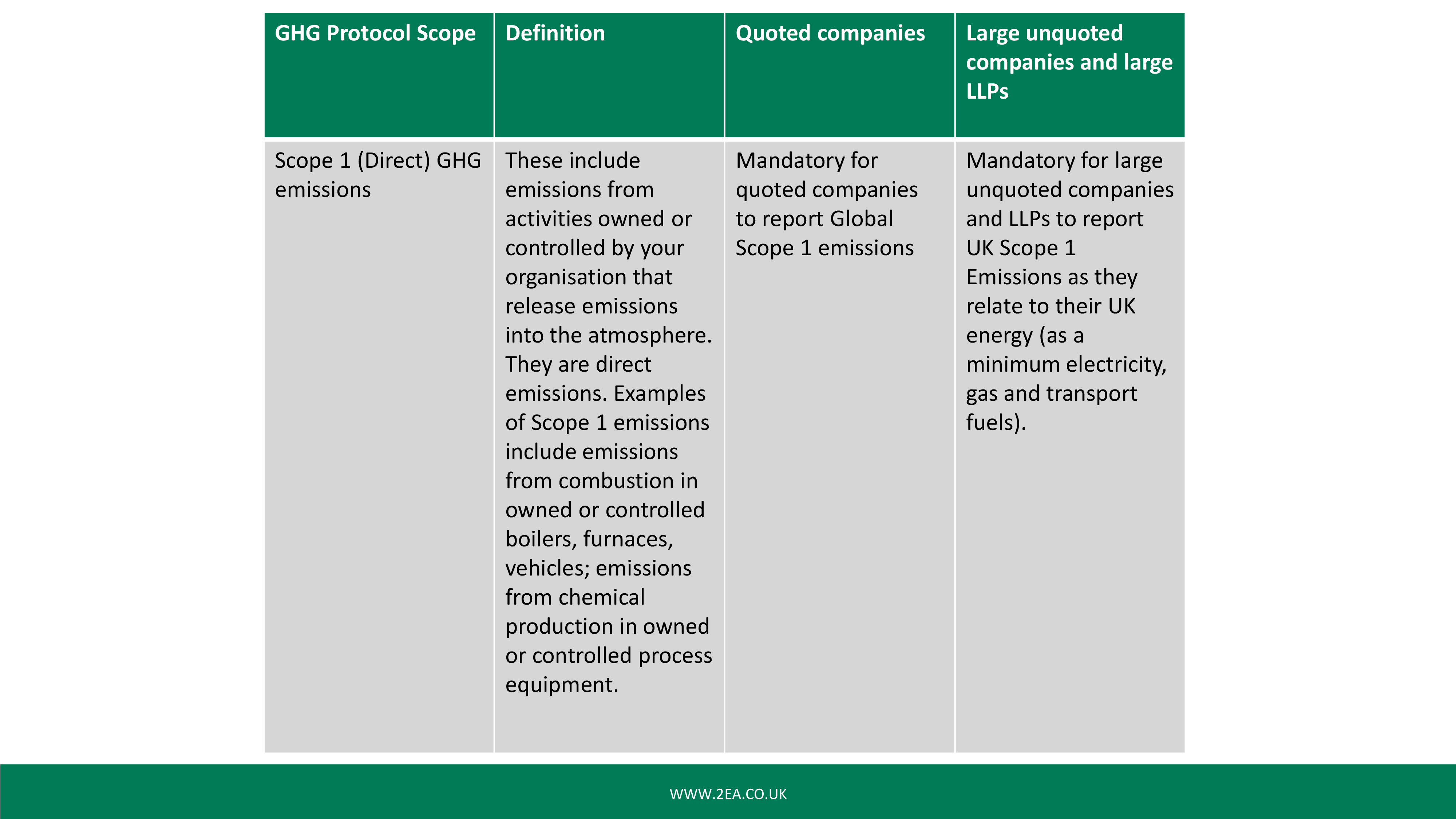

GHG Emissions Scope 1

So that brings us on to the GHG emissions. I’m guessing most of you already know most about this, but they are broken down in three scopes: one, two and three, and it is mandatory for both quoted and large unquoted companies and LLPs to include this scope within their SECR reporting. Again, if you go and get the guidance online from the website there are several pages that list every GHG for scope one, two and three in there – if I put them all in we’d be here for several hours and so I would have a look at that yourself.

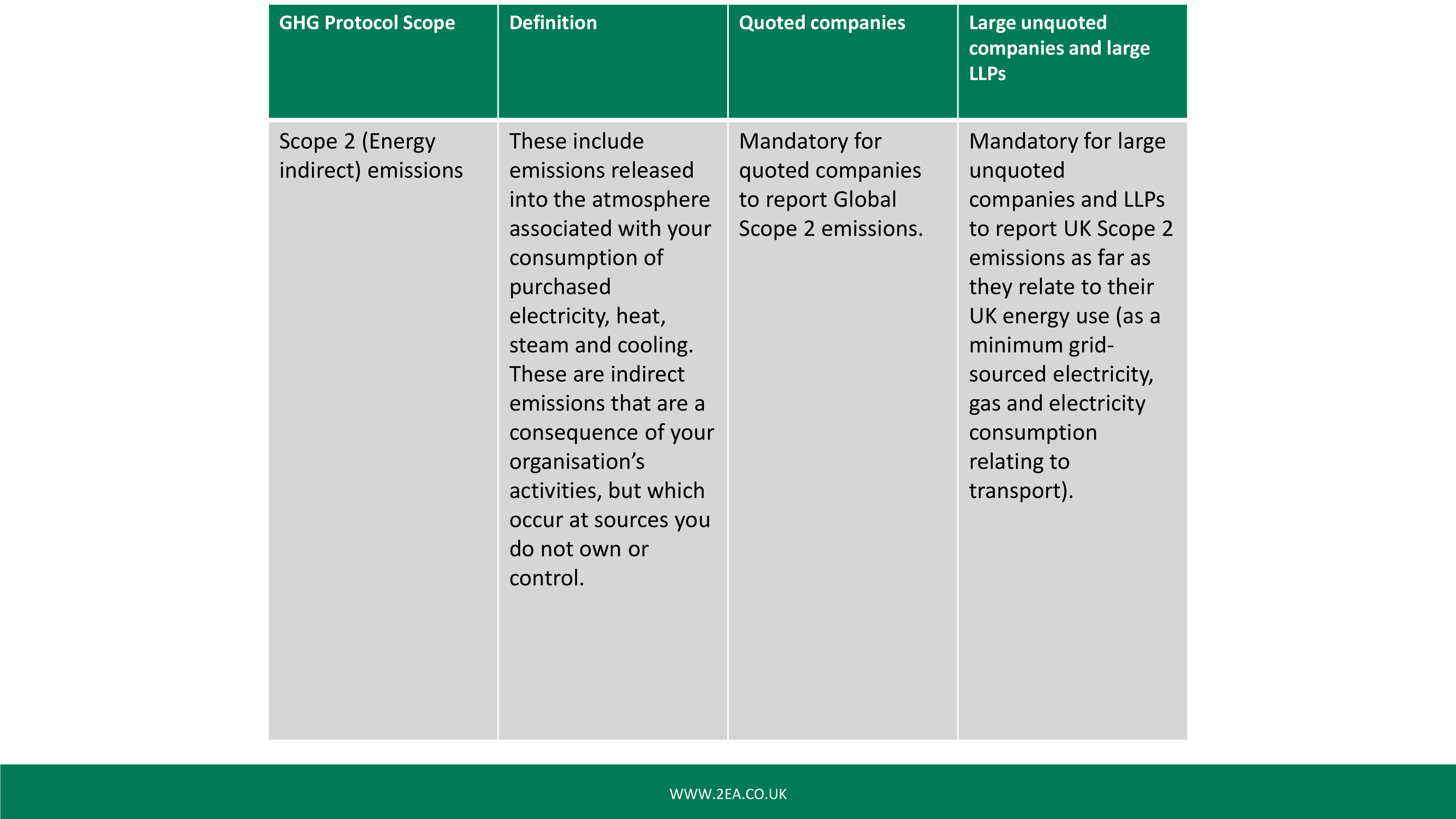

GHG Emissions Scope 2

You’ve then got scope 2, which is mandatory for quoted companies and mandatory for large unquoted companies.

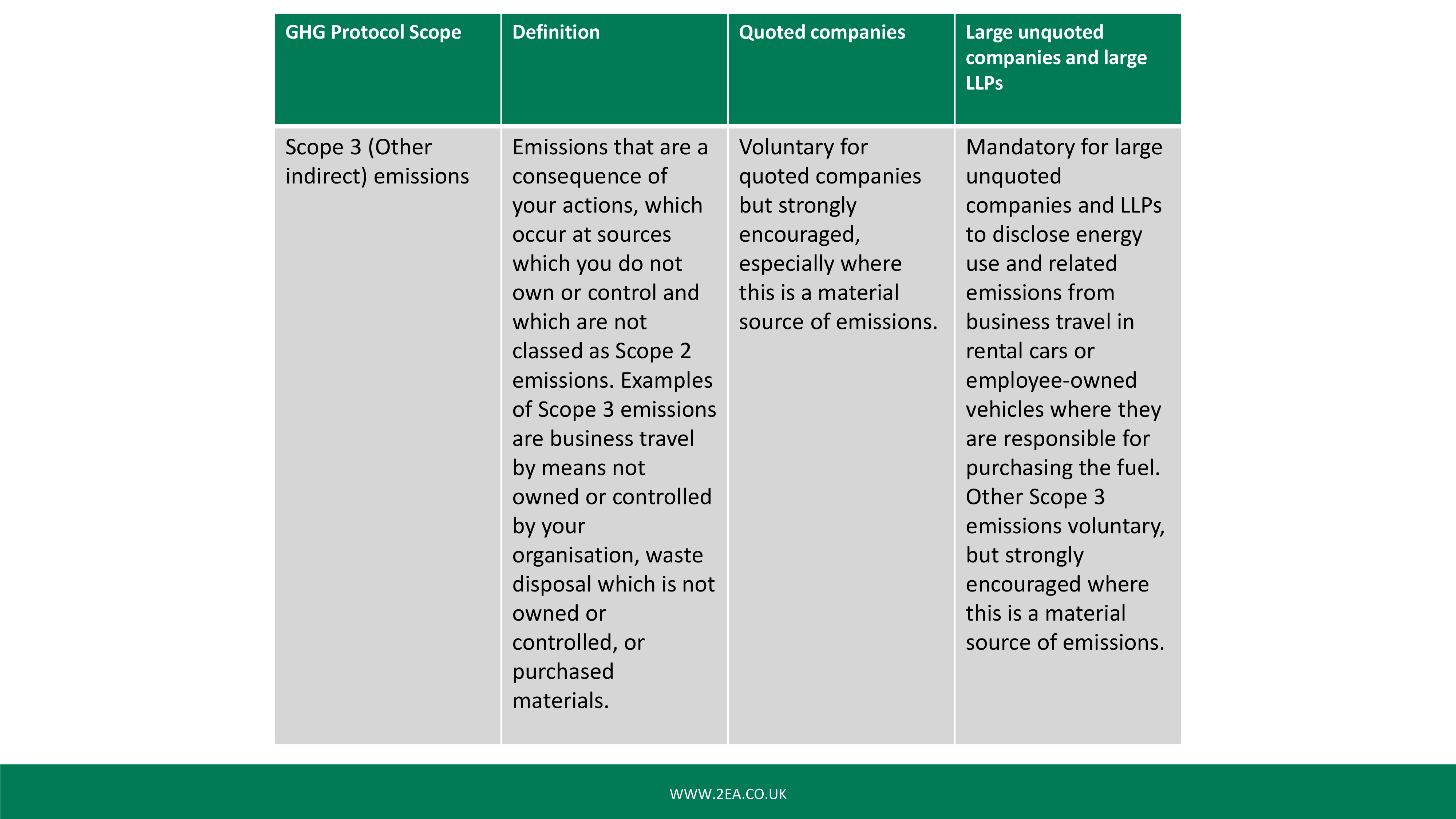

GHG Emissions Scope 3

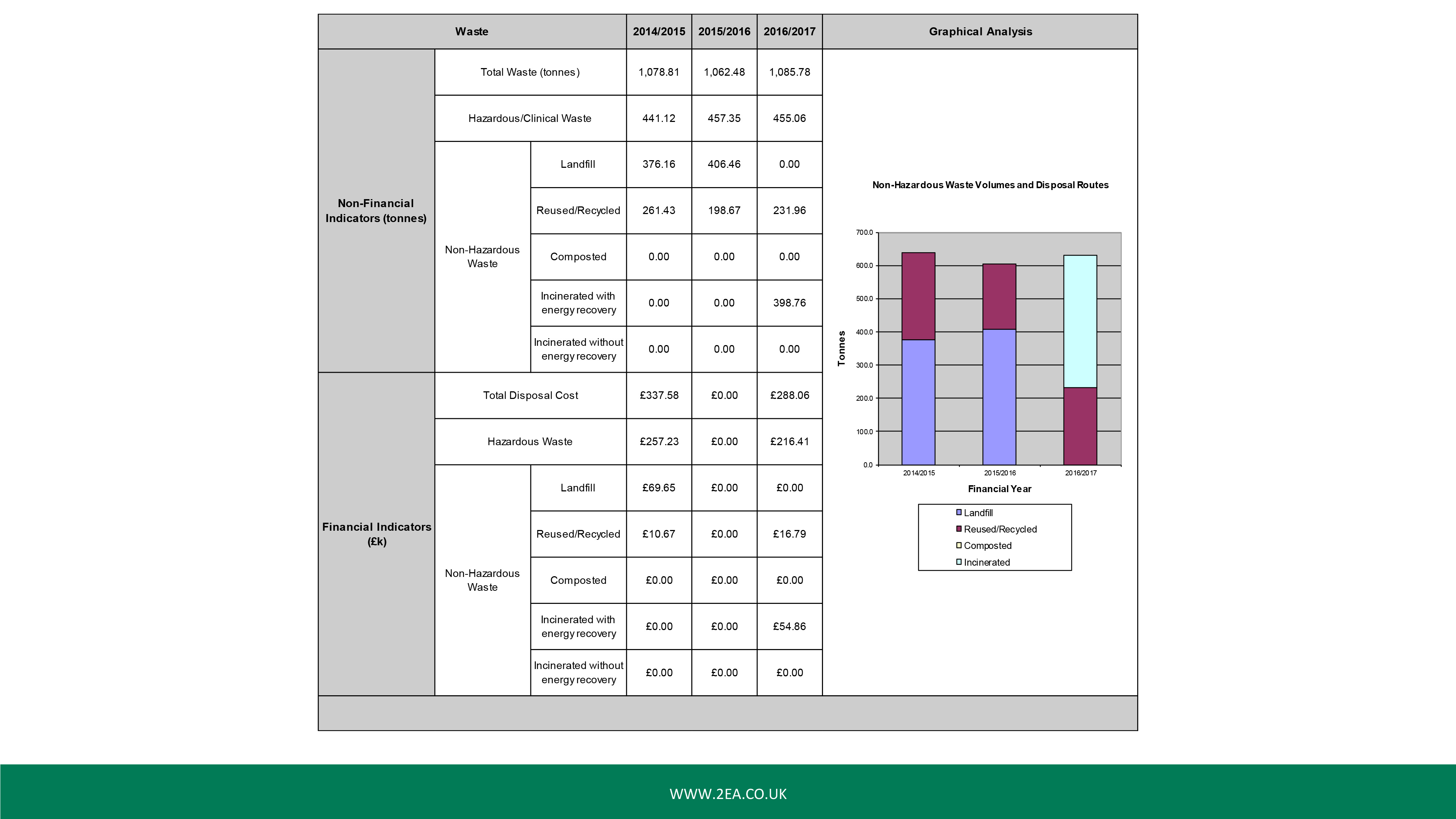

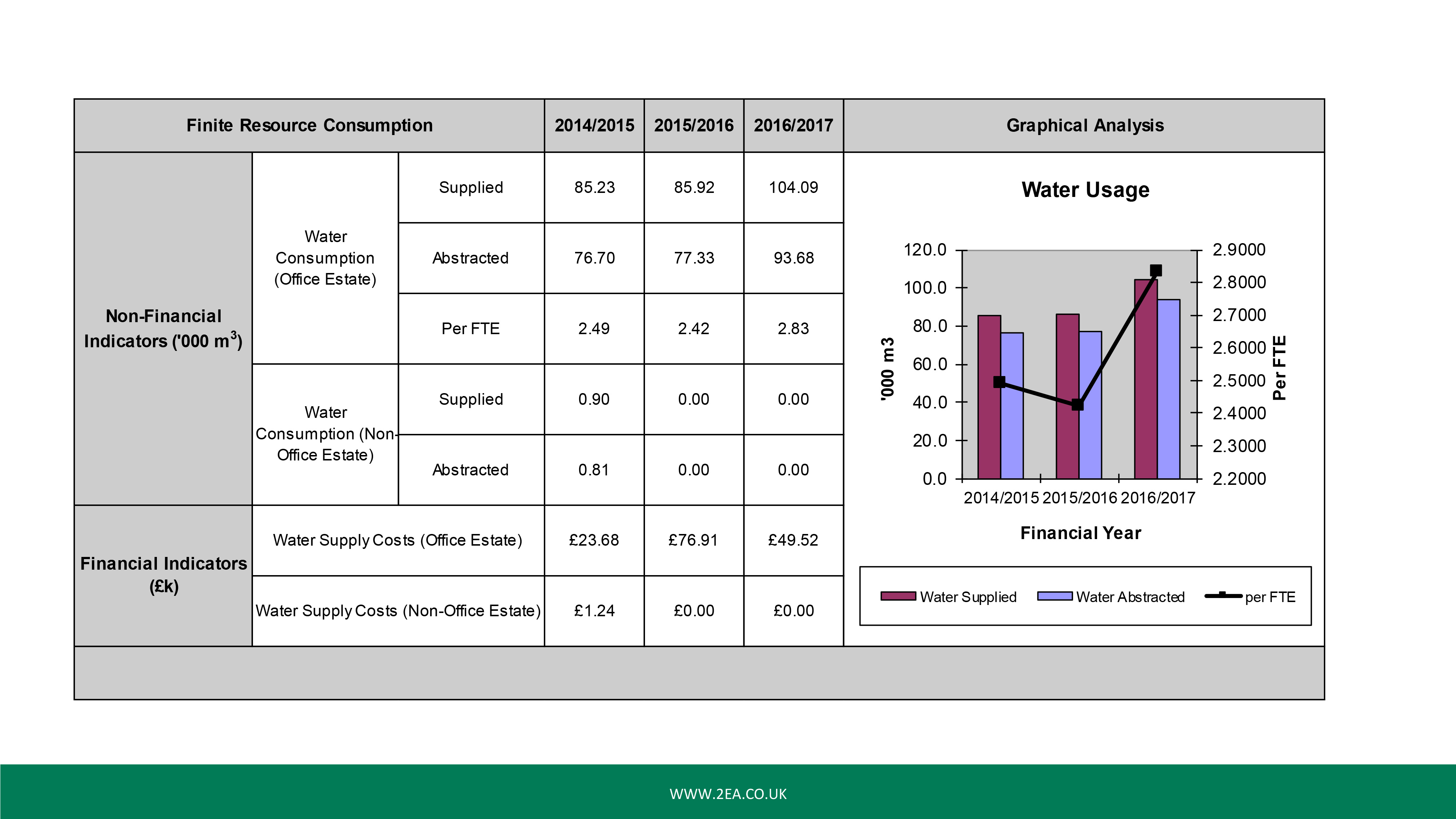

You’ve then got scope three, and this is where, for quoted companies, this is voluntary but for large unquoted companies and LLPs some of this is mandatory. Similar to ESOS and other frameworks, you can include things like water and waste but they’re currently voluntary.

We do think, especially the way it’s going, that eventually water and waste might be made mandatory reporting. And, as an energy management consultant, I would say that if water or waste plays a big part in your operations it might be advisable to include that data in your report.

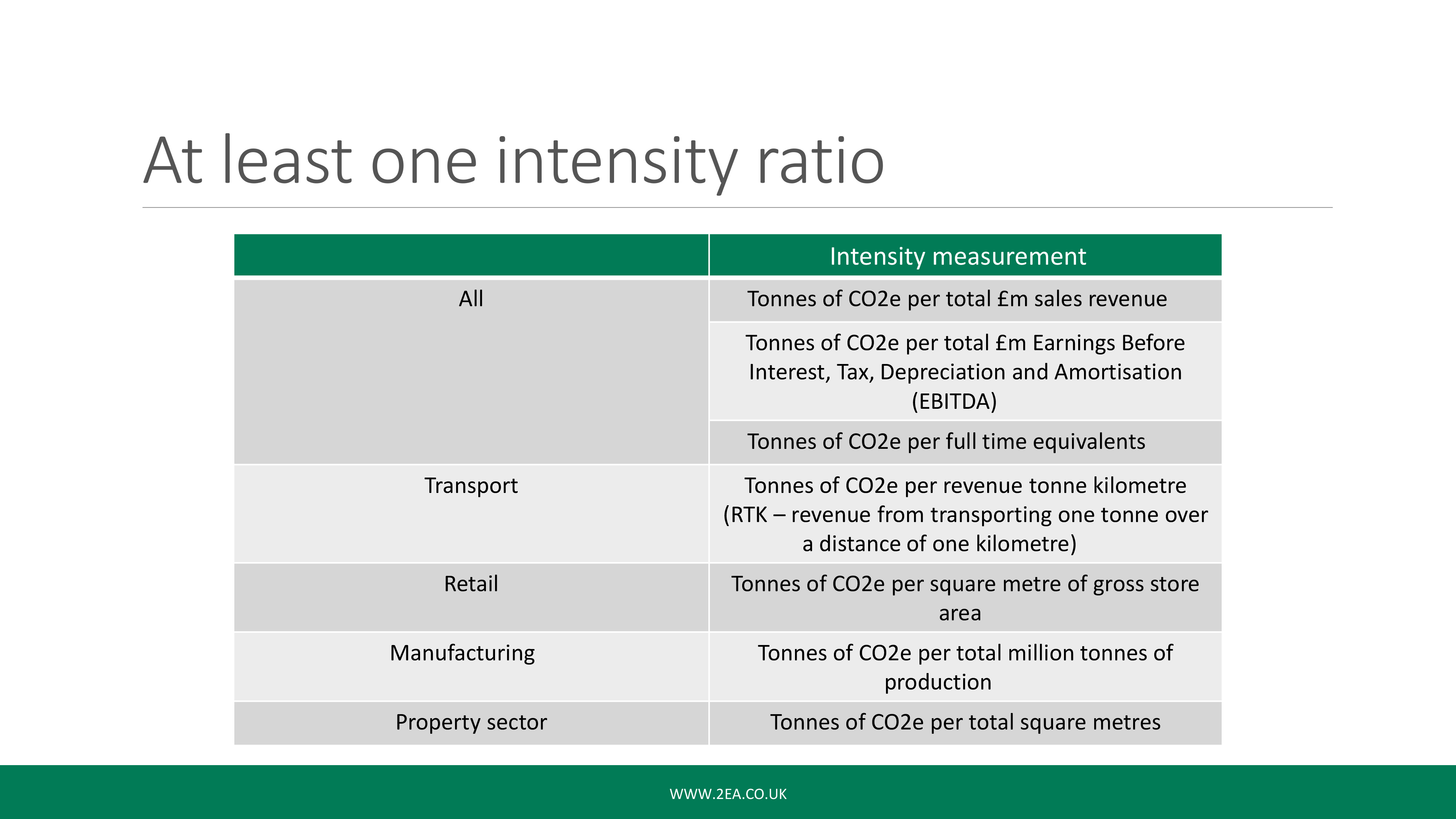

At Least One Intensity Ratio

The next one within that table is at least one intensity ratio. As the intensity ratios compare emissions data, again these are in the guidance and, I’ve taken a few to give you an idea, but you can put your emissions against the ones on the screen. There’s ones for most main sectors and obviously this allows comparison of energy efficiency performance over time. The report, again, must state at least one intensity ratio. You can use more, and you can feel free to use one that isn’t in the guidance that you might already be using within your organisation but, again, they want at least one.

Energy Efficiency Action Taken

The next one is energy efficiency action taken. There’s not a lot in the guidance that really talks about this. What this means is it’s for you to put in the report whether you’ve actually conducted any actions in relation to energy efficiency. That can include things like having a consultant go in and audit your building or that you can say “well actually you know last year we put in LEDs”, you can include that in your report and the government would like to see something in there to show that you have identified savings. But that’s up to you at the end of the day. If you haven’t done anything, again, as a consultant, I would advise that you either do it in-house or get an independent consultant to come in and identify energy-saving measures because they can save you a bit of money.

Methodologies

The next one is methodologies and this is the final one. So, while there’s no prescribed methodology under the legislation, organisations are required to disclose a methodology. They use an example on there but, again, you must state in your report what methodology or methodologies are used. There are no set criteria of which one you have to use if you’re already using one you can carry on using that one and explain it in your report.

Your SECR Report

Which brings us onto our report. So, there is again no prescribed reporting framework. You can just develop your own format to fit in with your business but you need to at least have a minimum of the information that we’ve covered today.

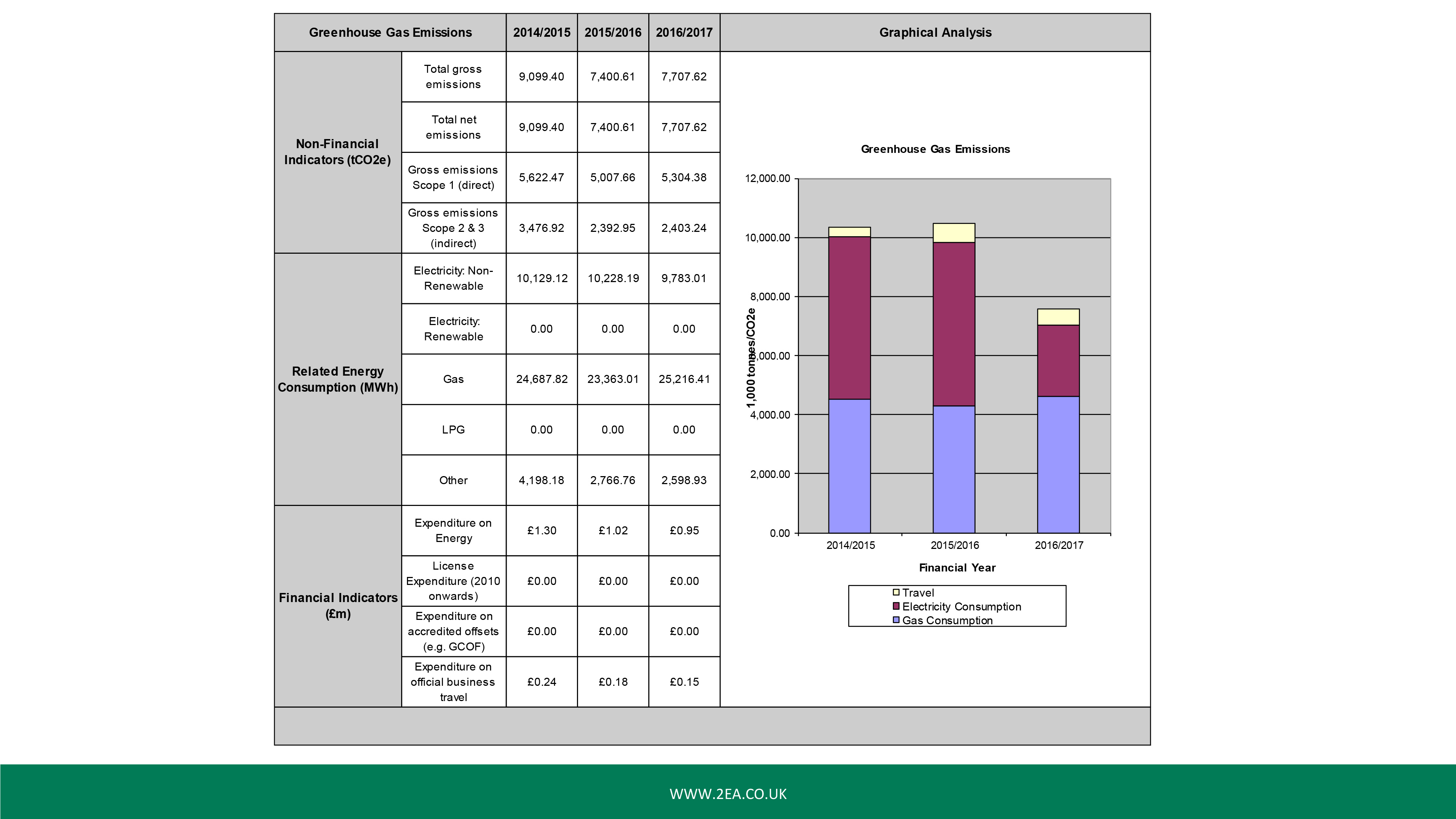

What you see on screen is what we put into our reporting. This kind of gives you an idea of what you, as a baseline, need to put in your report and I’ll leave it up there for a minute while you have a quick read through.

Cool. These are examples of the way in which you could create your SECR report and I will say this: your SECR report does not have to be hundreds and hundreds and hundreds of pages. The classic “keep it simple” kind of thing works. Get the information in there you need to report on.

There’s another image and these are actually taken from the guidance. If you have a look through the guidance, a lot of it is there to help you get it done correctly and in the right way without too much wasting of time.

There’s another one with an example of water. Again, water is currently voluntary but, as I said, we would recommend that you consider adding it to your report.

Key Takeaways

So that’s kind of a quick run-through of SECR. Here’s a couple of main key takeaways to remember:

- Two or more: 250+ staff, turnover £36m+, annual balance sheet £18m+

- Subsidiaries can report themselves unless part of group reporting

- Low Energy User = 40 MWh or less

- Use data from CRC scheme, ESOS, CCAs and MHGH reporting frameworks

- UK energy use, associated GHG, one intensity ratio, energy efficiency actions & methodology used

- Make sure you have the right resources in-house or hire a consultant

Remember, SECR will be submitted to Companies House through the following accounts. We know the Environment Agency isn’t involved in this, this is purely BEIS and reporting through Companies House, if you aren’t experienced with Companies House, there is a chance that people will be able to view this report or a slimmed-down version of this report so that is a key thing to think about because people will now be able to see how well you are performing on an energy and environmental scale.

I’ll put the slide of the flowchart up there and when we send the slides out, I can send you that flow chart as a single sheet if you require.

So I hope that all kind of made sense and I hope I didn’t go too fast for you all. I’ll include a link to the PDF presentation below for you to look at in your own time. In the meantime, if you have any questions, please feel free to email info@2ea.co.uk.